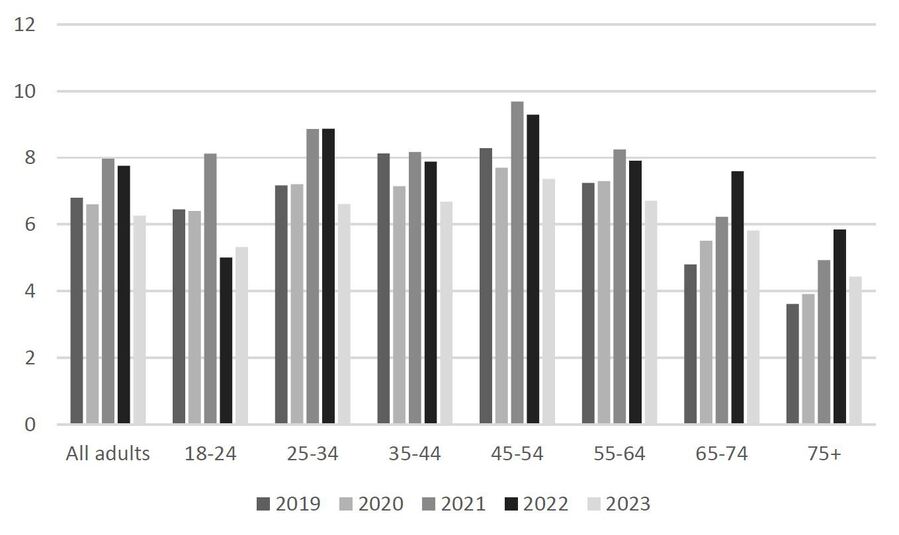

Older adults are often viewed as more susceptible to scams, but it is only since the pandemic that they have started to account for a significant proportion of victims, as figure 1 below illustrates. It is still the middle aged that account for the most victimised age group, but older adults tend to lose more and victimisation often leads to wider emotional, health and financial consequences, which many find it difficult to recover from.

Figure 1. Percentage of age groups victims of fraud in England and Wales.

Note, from 2023 the 18-24 age group expanded to 16-24.

Preventing scams against older adults is therefore a very important subject and given many older adults have a different attitude and use of technology different approaches to the young and middle-aged are required. Researchers at Portsmouth University in the UK have been involved in two projects looking to identify better ways to prevent scams against older adults.

The first project was jointly conducted with researchers in South Korea. The researchers first sought to map what strategies are in place in the two countries to prevent fraud against older adults. The researchers identified over 75 schemes and products which are directed either specifically at fraud prevention against older adults or a fraud they fall for in significant numbers. These were divided into four categories:

Traditional crime prevention applied to fraud: spyholes, signs, risk assessments etc:

Awareness and behaviour related prevention schemes targeted at fraud: general campaigns, tailored campaigns, reverse scamming etc.

Protection using modern technologies to prevent fraud: video doorbells, call blockers etc

Protections using 4th industrial revolution technologies to prevent fraud: spam email detection, phishing detection and advanced call blocking

A full list of the key tools can be found here . What was surprising was that even in Korea where technology is much more dominant. There were few technological solutions using the latest fourth industrial revolution technologies. Fraud prevention for older adults is still under-developed and utilises traditional crime prevention techniques applied to fraud.

Further the research found there was very little evaluation of fraud prevention. The paper that explores this is published here . The researchers also sought data on what practitioners think work using both a survey and interviews. This work is still under review and will be published later in the year.

The discussions and research among the researchers did stimulate the development of a model to tackle fraud against older adults which is presented here which identifies individual measures targeted at the older adult, community and government measures and organisational strategies.

The older adults holistic prevention model

INDIVIDUAL MEASURES Understanding the risks and protections Conducting risk assessment Continuous scam awareness (CSA): attending regular awareness training, ongoing reading of relevant resources (articles, websites, leaflets etc), receiving general alerts Personalised alerts (alert of unusual activity on accounts/credit file or frauds occurring data predicts they are at risk of)

Protecting the physical and digital habitus Video doorbell (ideally smart and linked to facial recognition alerting client if face associated with potential doorstep fraud) Personal alarms with communication for immediate triage Call blockers for mobile and landline (smart) Appropriate virus protection and spam filters on devices Apps/software that automatically profile risk of websites, emails, SMS etc alerting individual For most vulnerable, third party monitoring of accounts (partner, family, professional)

Enhancing social networks and well being Pursuing social activities socially prescribed Encouraging discussion of scams |

↓

Individual older adult |

↓ ↓

COMMUNITY MEASURES (NGO/POLICE/GOVERNMENT) Identifying the vulnerable and mapping the risks Finding vulnerable older adults and supporting Offering risk assessments Fraud resilience advice Training professionals dealing with older adults to recognise potential risks and report Contacting persons who may have fallen victim to warn of further payments

Improving understanding of the risks and ways to protect Fraud awareness training/materials/websites etc Helplines Provision of alerts based upon latest intelligence targeted to appropriate groups Trusted trader lists Reverse scamming

Protecting the physical and digital habitus of older adults Provision of fraud prevention products to those who cannot afford

Improving social networks Social prescribing Provision of support groups

Smart regulation Smart regulations to reduce opportunities for fraud

Disrupting fraudsters Detecting and punishing fraudsters |

ORGANISATIONS PROVIDING KEY SERVICES (FINANCIAL INSTITUTIONS, TECH COMPANIES AND TELCOS) Identifying risks in transactions, interactions, vendors and customers Finding vulnerable older adults and supporting Training staff to identify potential fraud victims and intervene Smart monitoring of financial transactions to block or further triage Smart monitoring of telephone calls to block or warn customers Smart monitoring of other forms of communication to block or warn customers Smart monitoring to block fraudulent vendors Joined up monitoring (data-sharing real-time), such as telephone and banking data Improving understanding of the risks and ways to protect Fraud awareness training/materials/websites etc Helplines Provision of personalised alerts based upon profile, activities and accounts

Disrupting fraudsters

|

The model illustrates protecting older adults from fraud requires a multi-layered approach. First, individuals should assess their own risks using resources or professional help. Continuous Scam Awareness (CSA) through training, alerts, and AI-driven warnings can enhance protection. Future developments could include AI-powered fraud alerts based on online behaviour. Physical and digital security should also be improved—video doorbells with facial recognition, smarter call blockers, and AI-monitored wearable alarms could detect scams in real-time.

Community involvement is crucial. Police, NGOs, and governments should identify vulnerable individuals, offer training, and share intelligence to prevent scams. Awareness campaigns, tailored fraud alerts, and financial assistance for security tools can further safeguard older adults. Supporting social participation can also reduce loneliness, a key risk factor for fraud.

Companies, particularly banks, telecoms, and tech firms, play a critical role. AI and data-sharing could detect risky transactions and intervene before fraud occurs. Financial institutions can train staff to recognize and act on suspicious activities.

Finally, collaboration across sectors—community organisations, businesses, and law enforcement—is essential. Improved data-sharing and coordinated efforts can create a unified fraud prevention system, ensuring consistent messaging and proactive protection for older adults and most importantly identifying those at risk through sharing data and protecting them before they are victims.

Preventing fraud against older adults also requires communication with them and in another study we explored the best way to get fraud prevention messages to them. Based upon quantitative data from a survey and qualitative data from interviews with older adults and volunteers/workers working with older adults on a specific project. The most effective means to developing anti-scam messaging is one-to-one via friends and family. The media is also important through television and radio. However, perhaps the most important finding of all is that many older adults note not receiving any useful advice in the prior six months. In an age of everchanging frauds and mass targeting, this is very worrying and clearly the counter fraud community must do more to get over appropriate scam prevention and awareness communications to the most vulnerable groups in society more regularly.

These two studies provide some early foundation research to build on for other researchers and practitioners fighting scams against older adults. A surprising finding is the lack of research on preventing fraud in general and older adults specifically, particularly high-quality evaluations of what works. Clearly as a global anti-scam community more evaluation of initiatives is required so we can deploy the most effective solutions to protect this important group in society.

A database of fraud prevention products and services relevant to older adults

Research funded by ESRC Grant number ES/W011085/1

Bitdefender Report Reveals How Scams Operate Across Digital Channels

Bitdefender’s Global Scam Intelligence Report 2026 shows how organised scam campaigns move across advertising, websites, SMS, messaging apps and voice calls to exploit trust at scale.

Beyond Compliance: Why Organisational Accountability is Critical for Consumer Protection

How the NDPC-Meta initiative could strengthen data protection, organisational accountability, scam prevention and consumer trust across Nigeria’s digital economy.

Why Mexico’s Anti-Scam Response Needs Cross-Sector Coordination

GASA Mexico Chapter's Sissi De la Pena explains why scam prevention in Mexico requires stronger coordination across finance, telecoms, platforms, government and civil society.

GASA Mexico Shares Scam Prevention Tips During the 2026 FIFA World Cup

GASA Mexico shares practical advice for football fans on avoiding ticketing, travel, phishing and payment scams during the 2026 FIFA World Cup.

Watch the Global Anti-Scam Summit Europe 2026 Session Recordings

Watch keynotes, panels, workshops, working group sessions and Scam Fighter Awards recordings from the Global Anti-Scam Summit Europe 2026 in Lisbon.

.jpg)

Public-Private Partnerships in Action: Key Takeaways From the Global Anti-Scam Summit Europe 2026

Key takeaways from the Global Anti-Scam Summit Europe 2026 on how public-private partnerships can strengthen scam prevention, intelligence sharing, regulation and victim protection.

Nomorobo Joins Scam.org to Shield Consumers from Fraudulent Calls and Texts

Nomorobo has joined Scam.org as a member partner, bringing call and text blocking technology into the platform to help consumers protect themselves from fraudulent communications.

Scams Continue to Rise in Germany: Two in Three Adults Encountered a Scam in the Past Year

The Global Anti-Scam Alliance (GASA), in collaboration with Worldline, has released the State of Scams Germany 2026 Report.