ABA, COBA Lead Australian Banking Sector to Mitigate AU$600 Million Annual Scam Losses

Author: Sam Rogers, Marketing Director, Global Anti-Scam Alliance

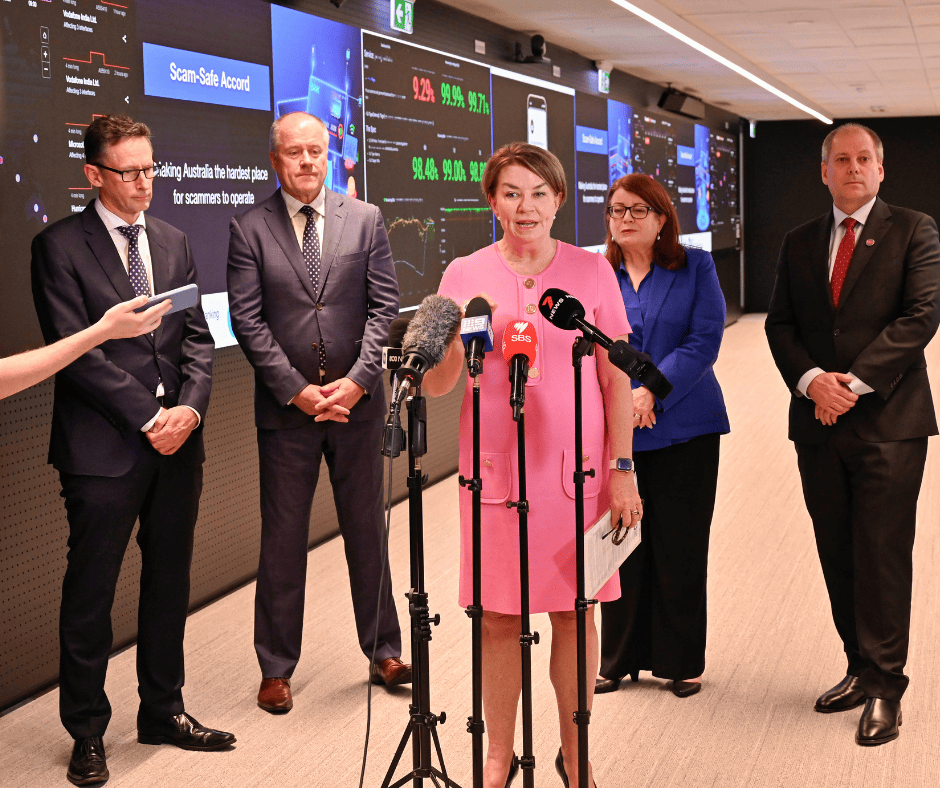

The Australian banking sector, in a commendable move, recently initiated the Scam-Safe Accord , a strategy aimed at significantly bolstering consumer protection against the out-of-control threat of financial scams. This accord, involving a range of community-owned banks, building societies, credit unions, and commercial banks, is an assertion by the industry that it understands its responsibility and has united its efforts to counteract fraudulent activities affecting its customers.

The Scam-Safe Accord: An Example of Consumer Banking Protection Done Right?

This move marks a strategic offensive in safeguarding Australian consumers and small businesses, defining the proactive measures every participating bank has committed to implementing. The essence of the Scam-Safe Accord lies in its framework, carefully put together to unite and fortify the Australian banking system against AU$600 million annual loss to scams from their accounts. So, what did the people behind this scheme have to say about it?

With the announcement of the Scam-Safe Accord, Anna Bligh , CEO of the Australian Banking Association (ABA) , was keen to point out that it is not only the banks who need to up their game, calling on “government, banks, telcos, social media, and crypto platforms” to work together on strategies against increasingly sophisticated criminal gangs.

Mike Lawrence , CEO of the Customer Owned Banking Association (COBA) , hailed the accord as a significant stride in the banking industry's ongoing battle against scams, pointing out that “governments, industry and consumers must remain vigilant to make Australia a hard target for scammers.”

It is worth noting that this trend of uniting industries is not confined to Australia. In 2024, the United Kingdom’s Payment Service Regulator (PSR) is scheduled to implement rules that require banks to reimburse scam victims within five days. The PSR also plans to publish data on how the top 25 banks are managing reimbursements and their levels of fraud. If successful, it is widely expected that this initiative will spread to the EU, and perhaps globally, before expanding to hold social media and big tech enterprises accountable for the abuse and scams that riddle their services.

Innovative Features of the Scam-Safe Accord

1. Confirmation of Payee System: A cornerstone of the accord is the introduction of a $100 million confirmation of payee system, poised to revolutionize payment security across all Australian banks. This system will crucially mitigate scam risks by authenticating the identity of payment recipients.

2. Enhanced Protective Measures: Participating banks will integrate more rigorous protective measures, including augmented warnings and payment delays for new or increased payment limits, a critical deterrent against precipitated scamming attempts.

3. Biometric Security Uplift: To counter identity fraud, the accord mandates an upsurge in technological and control measures, including the deployment of biometric verification for new account openings, thereby reinforcing customer identity security.

4. Sector-wide Intelligence Collaboration: A pivotal aspect of the accord is the expansion of intelligence sharing within the industry, with all banks engaging with entities like the Australian Financial Crimes Exchange (AFCX) by mid-2024. This collaboration is instrumental in sharing vital information about scam transactions.

Global Implications: Time for the World to Step Up and Unite

In an international context, the Scam-Safe Accord sets a new benchmark for consumer protection in the banking sector. Countries such as the United States and members of the European Union have made strides in combating financial scams, often through individual bank policies and regional regulations. However, the Australian banking sector and its Scam-Safe Accord is pioneering in its scope and execution.

Where Does It Measure Up Globally with Tried and Tested Anti-Scam Measures?

The Scam-Safe Accord aligns with several existing measures implemented by other countries and blocs. For instance, the emphasis on enhanced customer verification and identity protection mirrors the EU's strong focus on data security and privacy, as mandated by regulations like the General Data Protection Regulation (GDPR) . Similarly, the accord's initiative for biometric checks draws parallels with the increasing use of biometric authentication in America.

We have already seen countries like Singapore and Japan executing other stringent cybersecurity measures and public awareness campaigns to combat financial scams. The Scam-Safe Accord's focus on technological advancements, such as the confirmation of payee system, pitches up nicely alongside Asia's digital-centric approach.

Africa's approach to combating financial scams often revolves around community-based solutions and public-private partnerships. With a sizeable portion of the population using mobile banking, African nations like Kenya and Nigeria have developed innovative measures to tackle scams, including SMS-based alerts and fraud detection algorithms tailored to local contexts. Australia’s initiative could improve by including such community-focused strategies, potentially developing more grassroots-level awareness programs into its framework.

Where the Scam-Safe Accord stands out, however, is in its industry-wide approach. Unlike the sector-specific or individual bank policies often seen in the U.S. and EU, the Accord unifies an entire national banking industry under a common set of robust anti-scam measures. This timely implementation could also serve as a model for Asian countries where financial institutions are increasingly collaborating to tackle scams, especially in the face of rising digital payment fraud.

One might think the custodians of the world’s financial institutions should (and I’m sure, will) do well to monitor the results of the Scam-Safe Accord with great interest.

What Can the World Learn from the Scam-Safe Reforms Down Under?

In short, the global financial industry can take a lot from the Scam-Safe framework. The sector-wide intelligence sharing, for example, sets a precedent for more effective cross-bank and cross-border cooperation in scam prevention – something people were crying out for at the 2023 Global Anti-Scam Summit in Lisbon . In the U.S., where financial institutions often work in silos, a unified approach can enhance the effectiveness of scam detection and prevention.

The investment in the confirmation of payee system in Australia is another noteworthy aspect. While similar systems exist in parts of the EU, their implementation is not as widespread or unified. The U.S., meanwhile, could benefit greatly from adopting a similar system to reduce fraud in electronic payments.

The Scam-Safe Accord delivers a much-needed template for global financial institutions. As the overseers of the world’s financial integrity, it is imperative that global institutions observe and learn from the accord's implementation. Its success could herald a new era of international cooperation and unified strategies in the ongoing battle against financial scams.

By adopting similar collaborative and comprehensive approaches, countries around the world can not only enhance their own financial security but also contribute to a more scam-resilient global financial ecosystem. The Scam-Safe Accord is not just an Australian initiative but an example for global best practices in the fight against financial scams.

Australia Paves the Global Road for Scam-Safe Finance

Grounded in the principles of disrupt, detect, and respond, this new venture exemplifies the Australian banking industry's (and hopefully global) commitment to customer security. As a model of industry-wide collaboration and innovation, it presents a blueprint for other countries to emulate, signifying a substantial step forward in global efforts to mitigate financial scams.

As a lesson in collaboration, the Scam-Safe Accord is smashing through invisible barriers that are not only holding back the global banking sector, but many industries with a foot in the anti-scamming world.

Earlier I mentioned people are crying out for cross-border co-operation across government, law enforcement, national cybersecurity, as well as banking. If this works in the Australian banking sector, then who is to say law enforcement agencies around the world can’t find a way to replicate it with scam data sharing (yes, GDPR can be a serious obstacle in some cases); or National Cyber Security Centers (NCSCs) can share the “fingerprint” of prolific scammers to help their international contemporaries protect their own citizens.

We all need to watch the progress of the AFCX, since all ABA and COBA members will join by mid-2024. Is this not the precedential scam data sharing initiative that global scam fighters cried out for in Lisbon? An industry is leaving the comfort of their silos to go on an offensive against scams together – and I cannot wait to see the results.

On top of that, there is growing discontent with the disconnect between industries and those silos within them. The Scam-Safe Accord sets a high standard in consumer protection by attempting to get a stranglehold around the problem closer to the source (and certainly at the point of contact). It not only secures the Australian banking sector but also serves as an inspiring example for other industries and nations. The key factor being that “rivals” in any industry or geographical region can share knowledge that serves to protect all from a shared threat, for want of a better phrase, for the greater good and for the consumers who rely on them every day.

About the Author

Sam Rogers brings a diverse background to his role as GASA's Marketing Director. After working in Equity Capital Markets at a Big Four firm in the UK, he left in search of a creative role in the Netherlands. There, he specialized as a copywriter and marketing content creator, focusing on innovative fields of electrical engineering, including photonics and the industrial uses of electromagnetic radiation. Driven by a desire for meaningful impact, Sam pivoted from the industry sector to champion the cause against online scams, leveraging his skill set to raise global awareness about the detrimental effects of internet fraud.

What Really Works in Preventing Fraud Against Older Adults? Insights from Frontline Practitioners

Expert insights on preventing fraud against older adults, highlighting the role of technology, targeted education, bank intervention, and coordinated partnerships.

Brazil’s BC Protege+ Blocks Fake Bank Accounts Before They Can Be Opened

Brazil’s Central Bank launched BC Protege+, allowing individuals and businesses to block bank account openings in their name. With over 1 million activations, the tool offers a structural model for reducing identity-based fraud.

-1.jpeg)

From Vienna to Global Action: Key Takeaways from the UN Global Fraud Summit

Explore key insights from our participation at the UNODC's Global Fraud Summit in Vienna. Discover how AI is changing the scam landscape, the power of national anti-scam centres, and the introduction of the Public-Private Partnership Framework to protect communities from fraud.

League of Protectors: Women Fighting Against Scams

Explore key insights from our International Women’s Month webinar on combating scams. Discover how women leaders are driving cross-border collaboration, digital literacy, and collective action to protect communities from fraud.

The Real Gap in Fraud Defense Is Strategy, Not AI

Fraud losses keep rising despite advances in AI detection. The real challenge is fragmented strategy across banks, platforms, telcos and governments. Effective scam prevention requires coordination, shared signals and earlier intervention.

New Executive Order on Cybercrime and Fraud Marks a More Coordinated U.S. Response

A U.S. Executive Order targets cybercrime, scams, and global fraud networks with a more coordinated government response.

Global Anti-Scam Alliance Launches Scam.org with OpenAI and Key Partners

The Global Anti-Scam Alliance (GASA) launched today Scam.org, an AI-powered platform that provides scam education, prevention, detection, reporting, and victim support.

La Industrialización del Engaño: Por qué 2026 será el año en que las estafas cibernéticas cambien para siempre

El auge de la inteligencia artificial está eliminando las señales tradicionales de alerta y transformando las estafas en un sistema industrial a gran escala.